Key Takeaways

-

Stripe acquired Bridge for $1.1 billion in October 2024 — the largest acquisition in crypto history according to CNBC — and now supports USDC stablecoin payments in over 100 countries at a flat 1.5% fee.

-

More than 4.7 million businesses use Stripe as their payment processor in 2026. Adding crypto turns every existing Stripe integration into a potential gateway for stablecoins.

-

Stripe now offers four distinct crypto products: stablecoin payments, a fiat-to-crypto onramp, Stablecoin Financial Accounts (denominated in USDB), and Open Issuance for creating stablecoins via the Bridge API.

-

Stablecoins account for over 60% of crypto transaction volume in 2026 according to Chainalysis, with a total market cap exceeding $230 billion per DefiLlama — including more than $55 billion for Circle's USDC.

-

Bridge obtained OCC (Office of the Comptroller of the Currency) approval for a national bank charter in the United States — a significant regulatory milestone that gives Stripe's stablecoin infrastructure bank-level legitimacy.

Stripe and Crypto: From Ban to Billion-Dollar Bet

In January 2018, Stripe killed Bitcoin support on its platform. CEO Patrick Collison pointed to painfully long confirmation times and unpredictable network fees. Bitcoin simply wasn't built for the instant payment experience Stripe promised its 4.7 million merchants.

Seven years later, the reversal is dramatic. Stripe didn't just flip a crypto switch back on — the company dropped $1.1 billion on Bridge, built four native crypto products, and repositioned its entire platform around stablecoins. The bet is no longer on Bitcoin as a payment method. It's on stablecoins as programmable money infrastructure.

What changed? Stablecoins. Circle's USDC and Tether's USDT solved the volatility problem that made Bitcoin unusable in commerce. On networks like Solana, Base (Coinbase's L2), or Polygon, a USDC transaction confirms in under two seconds for fractions of a cent. That's faster than an ACH transfer and cheaper than a credit card swipe.

Patrick Collison summed up the thesis in one sentence: "stablecoins are superconductors for financial services." Stripe decided to treat them not as a crypto niche, but as a new global payment rail.

The Bridge Acquisition: Why $1.1 Billion?

In October 2024, Stripe announced it was acquiring Bridge, a startup founded by Zach Abrams (formerly of Square/Block). According to CNBC, it's the largest acquisition in crypto history — dwarfing Coinbase's 2018 purchase of Earn.com ($120 million).

Bridge isn't an exchange or a wallet. It's a stablecoin orchestration layer: an API that enables programmatic creation, issuance, transfer, and conversion of stablecoins. Before the acquisition, Bridge already operated the USDB stablecoin, used internally for cross-currency transfers.

Here's what Stripe actually bought:

-

Issuance infrastructure — the ability to mint stablecoins backed by verifiable reserves, which would become the Open Issuance product.

-

Regulatory licenses — Bridge already held authorizations across multiple jurisdictions to operate as an electronic money issuer.

-

The team — roughly 30 engineers specialized in the intersection of traditional finance and blockchain.

-

Conversion technology — near-real-time fiat↔stablecoin conversion APIs, now integrated into Stripe's crypto onramp.

The $1.1 billion price tag looks steep for a pre-revenue startup. But in Stripe's calculus — where the company processes hundreds of billions of dollars in annual volume — capturing even a few percentage points of that flow via stablecoin rails justifies the investment. Stablecoins represent over 60% of crypto transaction volume in 2026 according to Chainalysis, and their total market cap exceeds $230 billion as of early 2026 per DefiLlama. Stripe wants a piece of that flow.

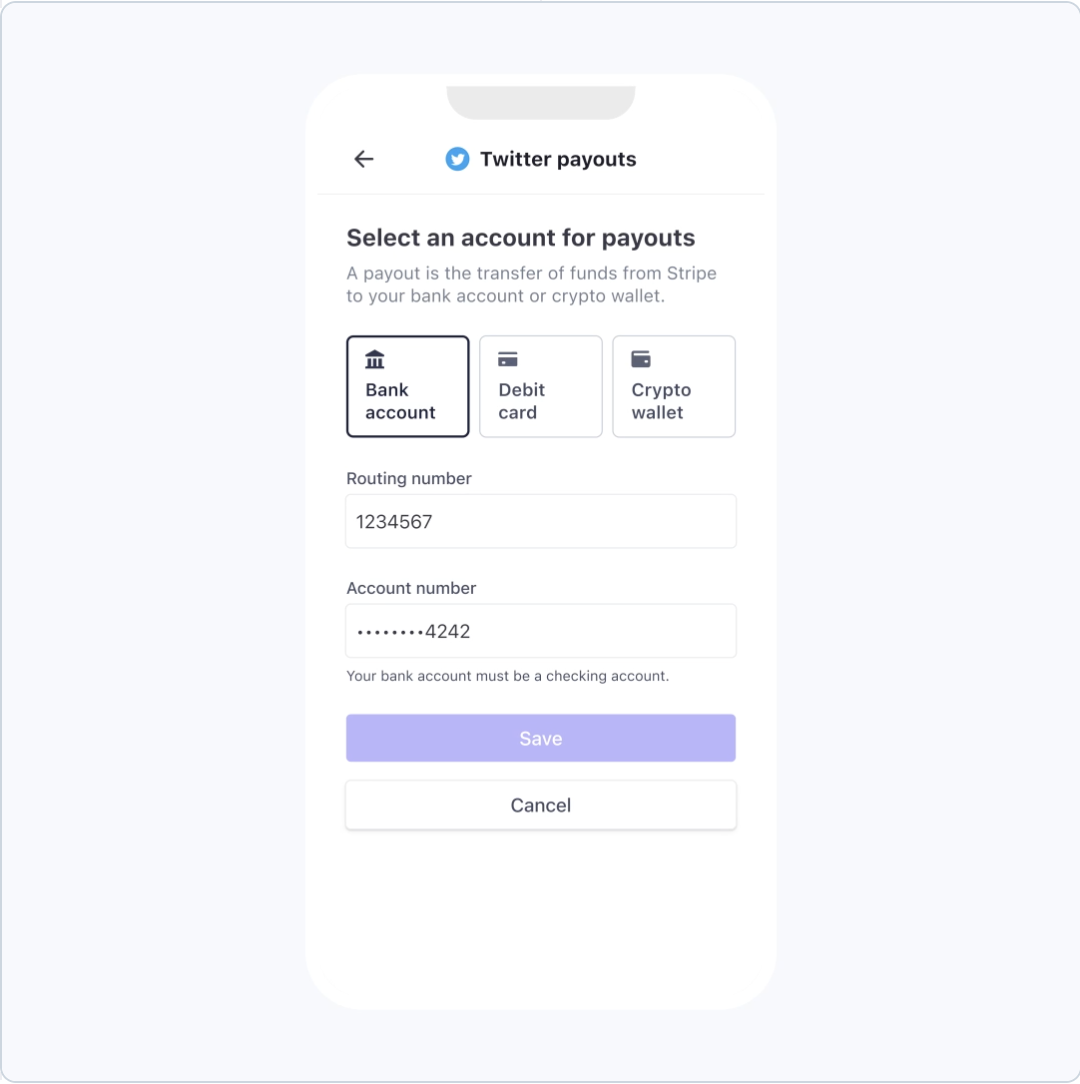

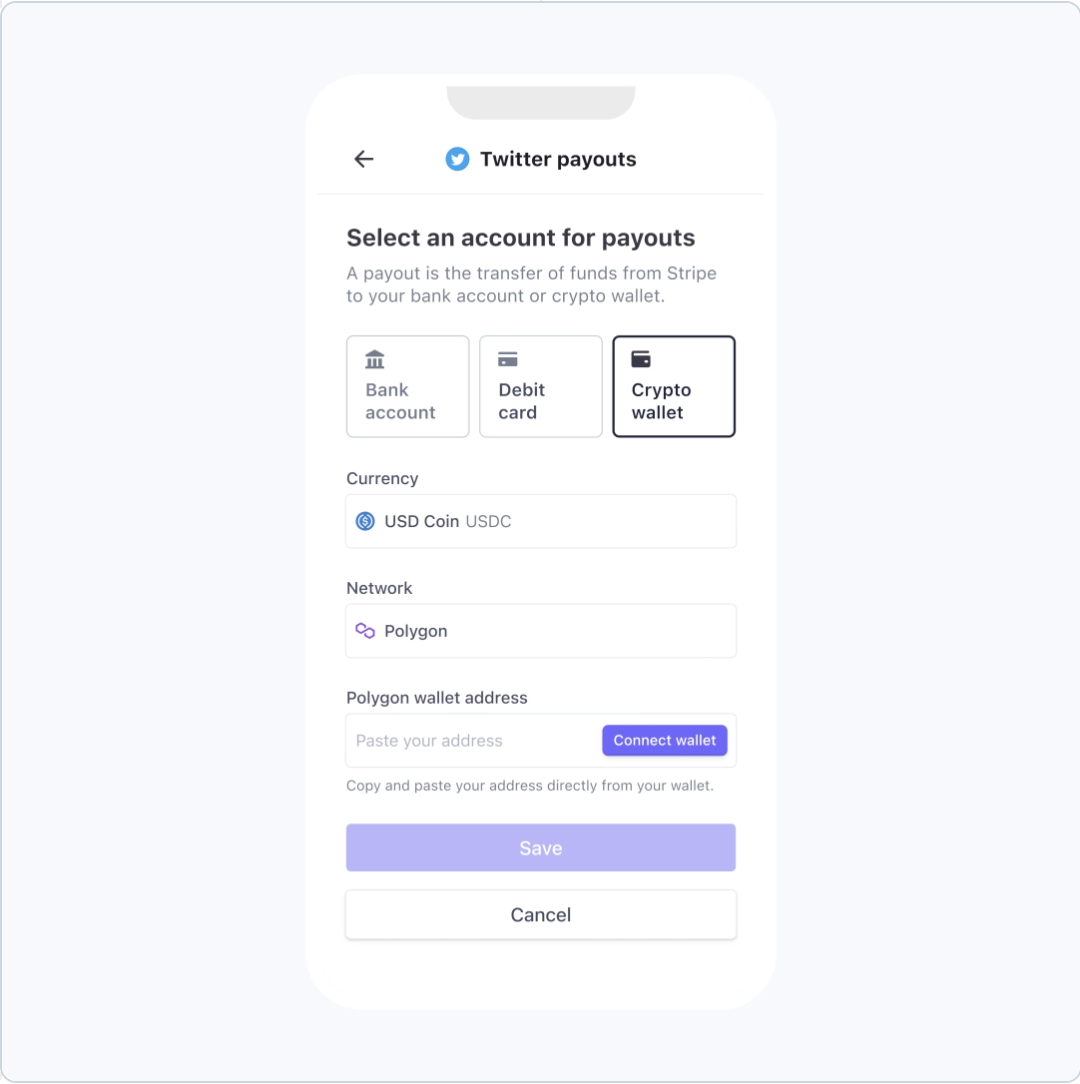

Accepting USDC Stablecoin Payments Through Stripe

Stripe's flagship crypto product lets merchants accept USDC payments directly through the existing Payment Element or the Checkout API. A merchant adds a "crypto" payment method to their Stripe integration, and customers pay in USDC from any compatible wallet.

Supported Countries and Settlement Currencies

Stripe supports USDC stablecoin payments in over 100 countries. US-based merchants receive settlement in USD by default. Merchants in the European Economic Area can receive settlement in euros, in compliance with the MiCA (Markets in Crypto-Assets) framework regulating stablecoins in Europe since June 2024. UK merchants settle under FCA oversight. Circle's USDC is one of the few stablecoins that meets MiCA compliance requirements — and in the US, Circle operates under state money transmitter licenses and has been positioning for SEC clarity — which is why Stripe chose to build exclusively on USDC.

The supported blockchain networks for receiving USDC payments are: Ethereum, Solana, Base, and Polygon. Settlement on the merchant side works one of two ways:

-

In fiat (USD, EUR, GBP, etc.) — automatic conversion, the merchant never touches crypto.

-

In USDC — the merchant holds the stablecoins in a wallet or a Stripe Stablecoin Financial Account.

For a US-based business, this is the key point: you can accept a USDC payment on Solana and receive dollars in your bank account in T+2, exactly like a standard card payment through Stripe.

The 1.5% Fee: What It Actually Covers

Stripe charges 1.5% per stablecoin transaction. For comparison, Stripe's standard US card processing fees are 2.9% + $0.30 for domestic cards. The stablecoin rate is significantly cheaper, especially on larger transactions since there's no fixed per-transaction component.

That 1.5% includes:

-

Blockchain network fees (gas fees) — Stripe absorbs these. The merchant pays nothing extra, even on Ethereum mainnet.

-

USDC→fiat conversion if the merchant opts for settlement in local currency.

-

Fraud risk management — Stripe Radar works on crypto payments too.

-

Unified reporting — stablecoin payments show up in the same dashboard as card payments, ACH transfers, or Apple Pay.

There's no setup fee, no monthly subscription, and no minimum transaction amount.

Step-by-Step API Integration

The integration follows Stripe's standard flow, with a few additional parameters.

1. Enable Crypto Payments in the Dashboard

In the Stripe Dashboard under "Payment methods," enable "Crypto — USDC." Stripe may request additional verification depending on your jurisdiction.

2. Configure the Payment Intent with the Crypto Method

const paymentIntent = await stripe.paymentIntents.create({

amount: 5000, // $50.00 USD currency: 'usd', payment_method_types: ['card', 'crypto'], crypto: { currency: 'usdc', networks: ['solana', 'base', 'polygon', 'ethereum'], }, });

3. Add the Payment Element on the Frontend

Stripe's Payment Element automatically detects the crypto method and displays a QR code or wallet connection button (MetaMask, Phantom, Coinbase Wallet, etc.). No additional frontend code is needed if you're already using the Payment Element.

4. Handle Confirmation Webhooks

Crypto payments use the same webhook events as traditional payments (payment_intent.succeeded, payment_intent.payment_failed). Confirmation is near-instant on Solana and Base (< 2 seconds), slightly longer on Ethereum mainnet (12–15 seconds).

5. Verify Settlement

Fiat settlement follows your standard Stripe account schedule. USDC settlement is available immediately in your Stablecoin Financial Account if you have one.

For merchants using Shopify or WooCommerce, the existing Stripe plugin supports crypto payments out of the box — just toggle the option in your settings.

Crypto Onramp: Convert Fiat to Crypto Inside Your App

Stripe's Crypto Onramp is a separate product from merchant payments. It lets any application embed a fiat-to-crypto conversion widget directly into its interface. The user enters a dollar amount, pays by card or bank transfer, and receives cryptocurrency in their wallet.

This product targets Web3 applications: blockchain games, NFT platforms, DeFi protocols, or any service that needs users to hold crypto. Instead of bouncing users to an external exchange to buy ETH, the app embeds the Stripe widget and handles conversion natively.

The onramp supports purchases of USDC, ETH, SOL, and other tokens on Ethereum, Solana, Base, and Polygon. End-user fees range from 2% to 3.5% depending on amount and payment method — competitive against alternatives like MoonPay (up to 4.5%) or Transak.

Technical integration uses an embeddable React component or a redirect URL:

const onrampSession = await stripe.crypto.onrampSessions.create({

wallet_address: '0x...user_wallet', destination_currency: 'usdc', destination_network: 'base', });

Stripe handles user KYC, regulatory compliance, and payment processing. The developer doesn't need a money transmitter license (at the state level in the US) or a VASP registration to integrate the onramp — Stripe carries the regulatory responsibility. In Europe, this means the developer doesn't need PSAN (France) or MiCA authorization either, as Stripe operates under its own licenses.

Stablecoin Financial Accounts: USDB-Denominated Accounts

Stablecoin Financial Accounts are the most ambitious piece of Stripe's new crypto stack. These are programmable accounts denominated in USDB — the stablecoin issued by Bridge, pegged 1:1 to the US dollar and backed by reserves held in US Treasury bills and bank deposits.

In practical terms, a Stablecoin Financial Account lets a business:

-

Hold funds in stablecoin without going through an exchange or external wallet.

-

Send and receive payments in USDB to/from any compatible wallet or another Stripe account.

-

Automatically convert between USDB and fiat (USD, EUR, etc.) via the integrated Bridge API.

-

Earn yield on the underlying reserves — Bridge passes through a portion of the Treasury bill yield to USDB holders.

This product is built for companies managing significant international cash flows. A marketplace paying contractors in 30 countries can use Stablecoin Financial Accounts to centralize its treasury in USDB, then convert to local currency at the moment of payout — avoiding traditional bank FX fees (often 2–3%) and the delays of SWIFT wire transfers (2 to 5 business days).

Open Issuance: Create Your Own Stablecoin via Bridge

Open Issuance is the most technical and forward-looking product in the lineup. Through the Bridge API, any company can issue its own stablecoin backed by verifiable reserves.

The goal isn't to create a competitor to USDC. Open Issuance targets specific use cases: tokenized loyalty programs, internal currencies for closed ecosystems (games, marketplaces), or regional stablecoins pegged to local currencies.

Bridge handles the technical infrastructure: on-chain issuance, reserve management, collateral audits, and compliance. The client company defines the parameters (name, symbol, deployment networks, redemption policy), and Bridge takes care of the rest.

This product is still in limited access as of early 2026, available only to companies approved through a due diligence process. In Europe, MiCA compliance imposes strict requirements for issuing electronic money tokens, which limits Open Issuance deployment in the EU to carefully regulated use cases. In the US, the SEC's evolving stance on stablecoins and potential stablecoin legislation in Congress (such as the GENIUS Act) will shape how broadly Open Issuance can be used domestically.

Security and Regulatory Compliance

Stripe Radar on Crypto Payments

Stripe applies its Radar anti-fraud engine to stablecoin payments with the same rigor as card payments. The analysis covers buyer behavior, sender wallet history, and transaction patterns. Each USDC payment runs through the same scoring rules as traditional payments, with no additional configuration required on the merchant side.

On the blockchain side, every transaction is publicly verifiable on the relevant network (Ethereum, Solana, Base, or Polygon). Stripe provides the transaction hash in the dashboard and via webhook, enabling a complete end-to-end audit trail — a level of transparency impossible with traditional card payments.

MiCA Framework in Europe

Since June 2024, the MiCA (Markets in Crypto-Assets) regulation governs the issuance and use of stablecoins in the European Union. Circle's USDC was among the first stablecoins to achieve MiCA compliance, with regularly audited reserves held in regulated financial institutions and segregated from Circle's corporate assets. In the event of issuer failure, holders have a right to redemption at par — a protection that didn't exist before MiCA.

Stripe, as a licensed payment institution in the EU, adds an additional compliance layer. European merchants don't need PSAN registration (France) or separate VASP authorization to accept stablecoin payments through Stripe — Stripe carries the regulatory responsibility.

Bridge and OCC Status in the United States

Bridge obtained approval from the OCC (Office of the Comptroller of the Currency) for a national bank charter. This approval — extremely rare for a crypto company — allows Bridge to operate as an electronic money issuer under federal banking supervision.

Stablecoins issued through Bridge (USDB and future Open Issuance tokens) benefit from a regulatory framework comparable to that of a traditional bank. For companies hesitant about using stablecoins for treasury management, this is a compelling argument: Bridge isn't an experimental crypto project — it's a regulated entity held to the same standards as a bank.

Real-World Use Cases: SaaS, E-commerce, and Freelancers

B2B SaaS with international clients. A software company billing clients in Latin America, Africa, or Southeast Asia constantly runs into the limitations of international wire transfers: 3- to 5-day delays, $15 to $40 per wire, and opaque exchange rates. With USDC payments through Stripe, the client pays from any wallet in seconds. The SaaS company receives USD in its bank account in T+2. Total fees: 1.5%, versus 3–5% for a SWIFT wire with currency conversion.

Shopify e-commerce. A Shopify merchant activates crypto payments in their Stripe plugin. Result: a new payment method appears alongside credit cards and Apple Pay at checkout. Crypto-native customers — who tend to be more loyal and have higher average order values according to BitPay data — can shop without friction. The merchant doesn't manage any wallet or handle any conversion. Everything flows through Stripe.

Freelance developer. A US-based developer working for Web3 startups in Singapore or Europe can receive payments in USDC through Stripe. Instead of waiting on a SWIFT transfer with intermediary fees, the payment arrives almost instantly. If the freelancer has a Stablecoin Financial Account, they can keep a portion in USDB (earning yield) and convert the rest to dollars as needed.

Services marketplace. A platform connecting contractors across 20 countries can use Stablecoin Financial Accounts as a treasury layer. Incoming payments convert to USDB, then get distributed to contractors with local currency conversion at the time of payout — all through the Bridge API, without touching a single bank wire.

Current Limitations and Things to Watch

Despite the ambition, several limitations deserve attention.

USDC only. For merchant payments, Stripe supports only USDC. No Bitcoin, no Ethereum, no USDT. It's a deliberate choice — stablecoins are better suited for payments than volatile assets — but it excludes a significant chunk of the crypto community that primarily holds BTC or ETH.

Dependence on Circle. The entire payment stack relies on Circle's USDC. If Circle hit regulatory trouble or a liquidity event (like the brief depeg in March 2023 tied to the Silicon Valley Bank collapse), all of Stripe's crypto payments would be affected.

Uneven geographic availability. While USDC payments work in 100+ countries, Stablecoin Financial Accounts and Open Issuance are more restricted. Local regulations — including MiCA in Europe, SEC guidance and potential stablecoin legislation in the US, and FCA requirements in the UK — create access asymmetries across jurisdictions.

Accounting complexity. In the US, accepting stablecoin payments and having them auto-converted to USD raises questions around tax treatment. Does the merchant need to recognize a crypto asset and then a conversion, or simply report the USD amount received? The IRS hasn't issued detailed guidance on this specific workflow, though under current rules, stablecoins are treated as property for tax purposes. Merchants should consult a crypto-savvy CPA to ensure proper reporting.

Irreversibility of blockchain payments. Unlike credit card payments (where chargebacks are possible for up to 120 days), a confirmed on-chain USDC payment is irreversible. Stripe handles refunds through its own system, but the underlying flow is fundamentally different from a card payment.

No in-store support. Stablecoin payments on Stripe are online-only for now. Stripe Terminal (their point-of-sale product) doesn't support crypto yet.

Frequently Asked Questions

Can Stripe actually let me accept crypto payments on my online store?

Yes. Merchants with a Stripe account can activate USDC payments and receive settlement directly in USD (or their local currency) in their bank account. Stripe handles the conversion automatically. In the US, Stripe operates under its own money transmitter and FinCEN registrations. In the EU, the MiCA framework governs USDC as a compliant stablecoin. Your country needs to be among the 100+ supported — the US, UK, Canada, and most of Europe are all covered.

How do Stripe's stablecoin fees compare to SWIFT wire transfers and card payments?

Stripe charges 1.5% per USDC stablecoin transaction, with no fixed component and no setup fees. An international SWIFT wire transfer typically costs $15 to $40 in fixed fees plus 2–3% in FX markup, with a 3- to 5-business-day delay. A card payment through Stripe costs 2.9% + $0.30 (domestic US) or up to 3.9% + $0.30 (international). For high-value cross-border transactions, stablecoins are the cheapest channel available.

How do I integrate Stripe's crypto onramp into my SaaS application step by step?

Integrating the crypto onramp requires a Stripe account with the crypto option enabled. You create an onramp session via the API, specifying the user's wallet address, target cryptocurrency, and network. Stripe provides an embeddable React component or redirect URL that handles KYC, card payment, and token delivery. Full documentation is available at docs.stripe.com/crypto/onramp.

Can I get paid in stablecoin through Stripe and receive dollars directly in my bank account?

Absolutely — that's actually the default behavior for US merchants. When a customer pays in USDC, Stripe automatically converts the amount to USD and settles to the merchant on the standard schedule (T+2 in most cases). The merchant doesn't need a crypto wallet and never holds any stablecoin if they prefer not to.

What's the difference between Stripe's Stablecoin Financial Accounts and a regular bank account?

A Stablecoin Financial Account is a programmable account denominated in USDB — Bridge's stablecoin pegged to the dollar. Unlike a traditional bank account, it runs on blockchain rails, enabling near-instant transfers to any wallet worldwide, 24/7. It also offers yield linked to the underlying US Treasury bills. However, it is not covered by FDIC deposit insurance (in the US) or the FSCS (in the UK). This is a critical distinction — your funds are backed by reserves, not insured by the government.

Are Stripe crypto payments available at physical point-of-sale terminals via Stripe Terminal?

Not yet. Stripe's stablecoin payments are online-only for now. Stripe Terminal — their in-store payment product — doesn't support crypto yet. For physical retailers, the only option is to use a QR code linking to an online Stripe payment link, which adds an extra step for the customer.

Will the Bridge acquisition change anything for developers already using the Stripe API?

For existing developers, the integration is seamless. The Bridge API is accessible as an additional module within the Stripe ecosystem — it doesn't replace any existing APIs. The new products (Stablecoin Financial Accounts, Open Issuance, crypto onramp) are optional and activated separately. That said, Bridge's infrastructure improves fiat↔crypto conversion performance under the hood, which indirectly benefits all Stripe users.